India’s financial system is entering a critical phase as policymakers attempt to balance strong domestic growth with rising global economic uncertainty, currency pressures, and shifting investment flows. While the Reserve Bank of India (RBI) continues to project confidence in the country’s macroeconomic fundamentals, recent developments in global markets and geopolitical tensions are forcing financial authorities to reassess risks tied to inflation, foreign capital, and long-term growth momentum.

Over the past several weeks, India’s financial and economic outlook has remained under close scrutiny after the RBI maintained its cautious monetary stance while simultaneously upgrading growth projections for the current fiscal year. The central bank has projected India’s GDP growth at 7.6% for FY26 under the revised GDP series, supported by domestic demand, manufacturing expansion, infrastructure spending, and resilient services activity. (DD News)

RBI officials have repeatedly emphasized that India remains one of the fastest-growing major economies despite increasing instability in global markets. Deputy Governor Poonam Gupta recently stated that the country’s macroeconomic conditions remain strong enough to sustain high growth alongside controlled inflation, even amid geopolitical disruptions and volatile energy prices. (The Times of India)

However, beneath the optimistic projections, policymakers are facing mounting external challenges. The Indian rupee has come under pressure in recent months as higher global crude oil prices, capital outflows, and uncertainty surrounding international trade routes weighed on investor sentiment. According to recent reports, the RBI and the central government are exploring measures to attract fresh dollar inflows to stabilize foreign exchange reserves and support the currency.

Among the options reportedly being evaluated are the revival of special foreign currency deposit schemes for non-resident Indians and tax adjustments aimed at encouraging foreign investment into Indian government bonds. The discussions come as India attempts to maintain reserve stability while navigating a difficult global financial environment shaped by rising geopolitical tensions in West Asia and fluctuating commodity markets.

Despite concerns surrounding the rupee, RBI Governor Sanjay Malhotra recently assured markets that India’s foreign exchange reserves remain adequate. India currently holds nearly $700 billion in reserves, sufficient to cover approximately 11 months of imports, according to central bank estimates.

Financial analysts believe the RBI’s confidence stems from relatively stable domestic consumption patterns, continued infrastructure investment, and the government’s broader fiscal consolidation strategy. The Union Budget for FY26-27 maintained a strong focus on capital expenditure while simultaneously targeting a reduction in the fiscal deficit to 4.3% of GDP. Economists say this combination is intended to sustain growth while preserving long-term fiscal discipline.

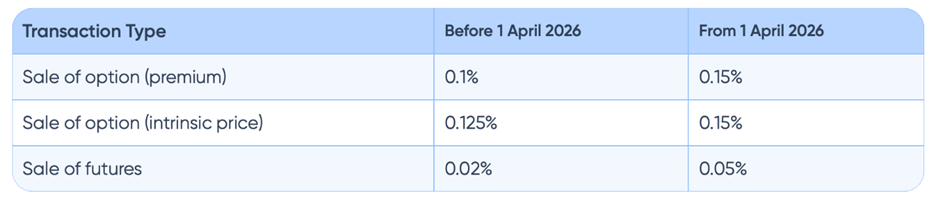

India’s financial policy environment is also evolving rapidly on the regulatory front. Beginning April 2026, several major financial reforms and taxation changes officially came into effect, impacting investors, traders, taxpayers, and digital payment users across the country. These changes include the rollout of the new Income Tax Act framework, revised taxation rules for Sovereign Gold Bonds, increased Securities Transaction Tax (STT) rates for derivatives trading, and expanded digital payment authentication requirements.

Data Source: Cleartax

Market participants say the reforms reflect the government’s attempt to modernize financial compliance systems while improving transparency and digital security across India’s rapidly expanding financial ecosystem.

India’s capital markets have meanwhile continued to attract attention globally. In recent years, the country emerged as one of the world’s most active equity fundraising destinations, supported by strong retail participation, digital trading adoption, and rising investor interest in sectors such as financial services, technology, renewable energy, and infrastructure. Recent RBI reforms allowing banks to expand acquisition financing and increase exposure to capital market activities are expected to further deepen corporate financing capabilities.

At the same time, economists remain divided over the sustainability of India’s investment cycle. While RBI officials maintain that private sector investment is strengthening alongside public infrastructure spending, some international institutions have raised concerns regarding slowing net foreign direct investment inflows and rising outward capital movement from Indian companies.

The International Monetary Fund (IMF) recently highlighted that despite India’s strong headline growth numbers, foreign direct investment momentum has weakened amid global uncertainty and changing international financial conditions. Analysts suggest that continued geopolitical instability, elevated U.S. interest rates, and supply chain disruptions could affect investment decisions in emerging markets, including India.

Inflation management also remains central to India’s financial outlook. Although retail inflation has moderated significantly compared to previous years, the RBI has continued to maintain a cautious approach due to ongoing risks linked to energy markets and imported inflation. The central bank recently reaffirmed the country’s inflation targeting framework, retaining the 4% target with a tolerance band of plus or minus 2% through 2031.

Financial markets are now closely watching whether prolonged geopolitical disruptions or commodity price spikes could eventually force the RBI to revisit its current monetary policy stance. So far, the central bank has chosen to maintain the repo rate at 5.25%, signaling that stability and inflation control remain priorities despite relatively strong economic growth.

Industry leaders believe India’s financial resilience will largely depend on its ability to sustain domestic demand while insulating itself from global shocks. Infrastructure expansion, manufacturing incentives, digital financial inclusion, and trade partnerships are expected to remain central pillars of India’s economic strategy through 2026.

Recent trade agreements with major global economies, including the European Union and the United States, are already being viewed as potential catalysts for stronger foreign portfolio inflows and long-term investment confidence. RBI assessments suggest that these agreements could improve both capital flows and export competitiveness over the coming years.

As global financial markets continue to navigate uncertainty around inflation, geopolitical conflict, and technological transformation, India’s policymakers are increasingly positioning the country as a relatively stable growth engine within the broader emerging market landscape.

The coming quarters, however, are expected to test whether India can maintain that balance between aggressive growth ambitions and financial stability in an increasingly volatile global economy.